ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

March 5, 2025 | Tit for Tariff Policies Weigh Heavy by Design

Danielle Park

Economic conditions today are more fragile than in March 2018 when Trump 1.0 signed a memorandum instructing the United States Trade Representative (USTR) to apply relatively modest tariffs of $50 billion on Chinese goods.

As RBC chief economist Frances Donald points out:

“In 2018-19, tariff policies raised the average import duty from 1.5% to approximately 3%. As of March 4, the average tariff rate quadruples to nearly 12%. That’s the largest trade shock to the U.S. and Canada since the 1930s.”

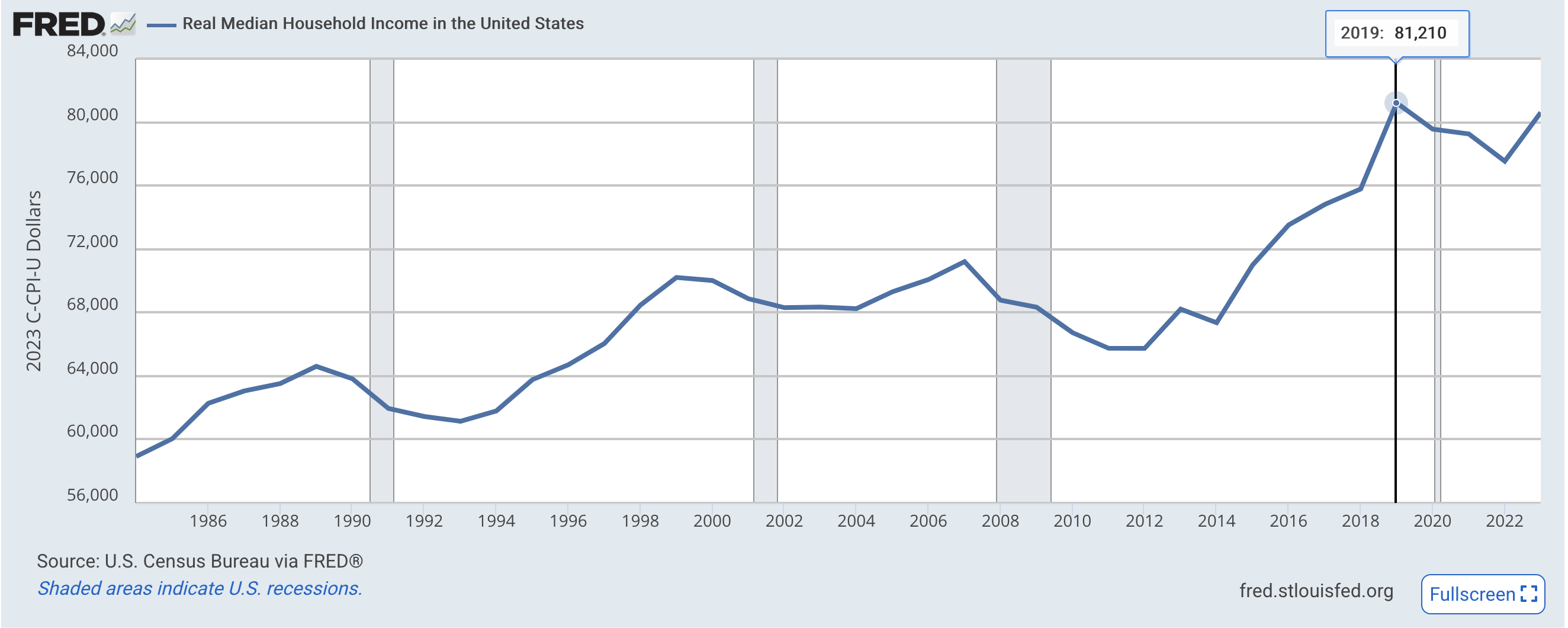

Since Trump’s first day in office in January 2017, the median real US household income has risen 10% from $74,810 to $82,373. Over the last five years, however, it has remained virtually flat at $81,210 in January 2019 (chart below since 1984).

At the same time, the median US home sale price rose 40.7% from $317,200 in January 2019 to $446,300 today, while the average 30-year fixed mortgage rate rose from 3.68% to 6.87%. The Fed’s overnight funding rate was .75 to 1% at the start of Trump 1.0, and it is 4.25% now. The 10-year Treasury yield was 2.44% versus 4.256% today.

At the same time, the median US home sale price rose 40.7% from $317,200 in January 2019 to $446,300 today, while the average 30-year fixed mortgage rate rose from 3.68% to 6.87%. The Fed’s overnight funding rate was .75 to 1% at the start of Trump 1.0, and it is 4.25% now. The 10-year Treasury yield was 2.44% versus 4.256% today.

At the start of Trump 1.0, the US housing affordability ratio was a healthy 166; today, it is sub-100 (98.5), meaning that a family earning the median household income does not have enough income to qualify for the median-priced house.

The average new car price in America rose 32.3% from $36,824 in 2019 to $48,700 at the end of 2024, while the average new car loan rate (48 months) rose from 5.39% to 8.49%.

The personal savings rate slumped from 6.2% to 4.5%, and debt levels leapt.

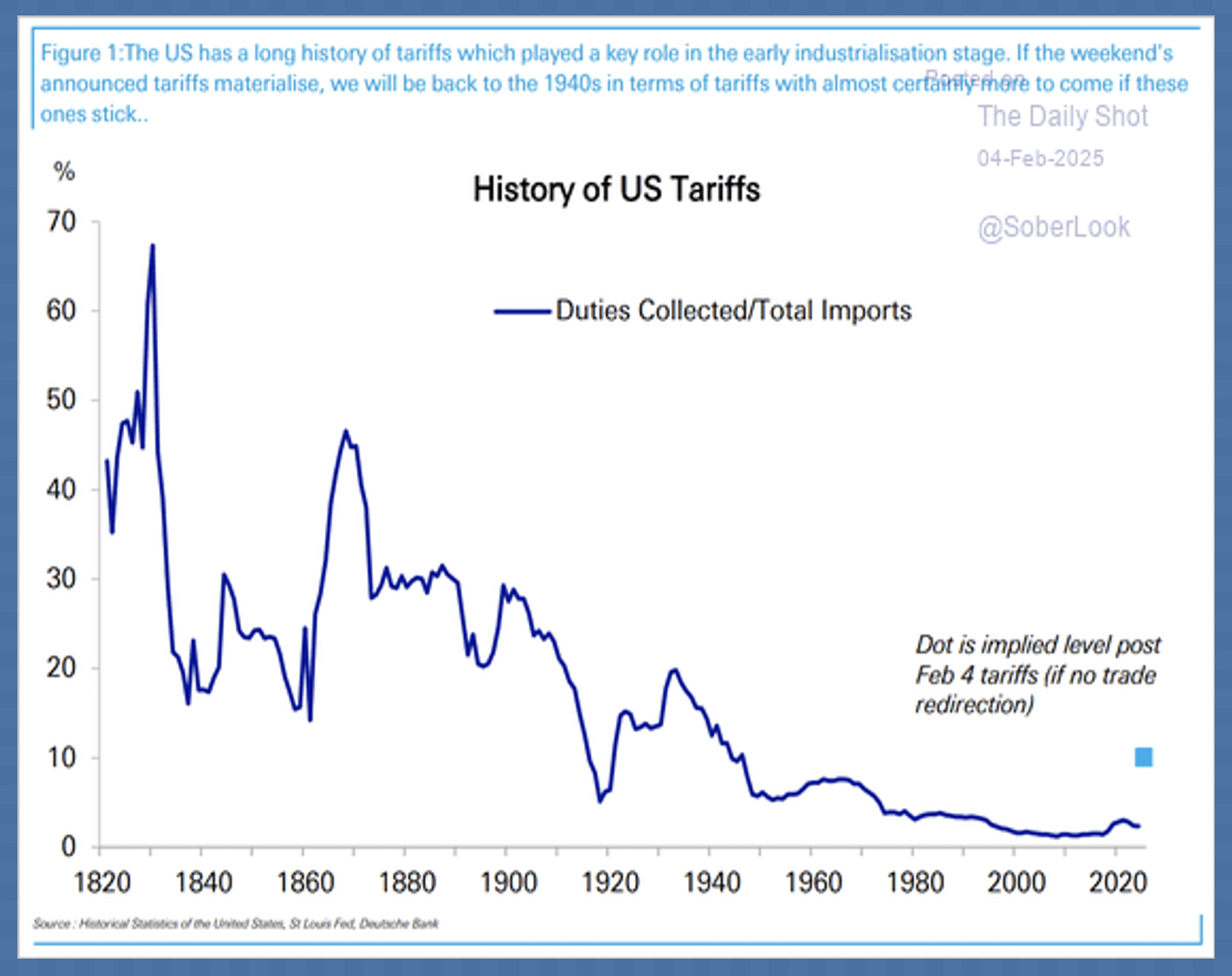

President Trump has seized on tariffs to help pay for more tax cuts, a concept which has played a recirculating role in American economic policy since the nation’s founding.

The history of US trade tariffs (shown above since 1820) is one of evolving strategies—shifting from revenue generation and protectionism in the early years to promoting global free trade in the modern era, with periodic returns to protectionist measures in response to specific economic challenges. We’re there again now.

How long and what tariffs persist is everyone’s guess, but the Bank of Canada (BoC) noted in its January 29, 2025 meeting minutes that sentiment damage is already done:

Members viewed the impact of prolonged trade uncertainty on business investment and consumer confidence as the main downside risk to the outlook. They discussed this at length. Even if no tariffs were imposed, a long period of uncertainty under the cloud of tariff threats would almost certainly damage business investment in Canada. Members discussed recent survey results from the Business Leaders’ Pulse and anecdotal information that indicated that some businesses were considering shifting investment to the United States. This would likely lead to negative effects on hiring, labour income and household spending.

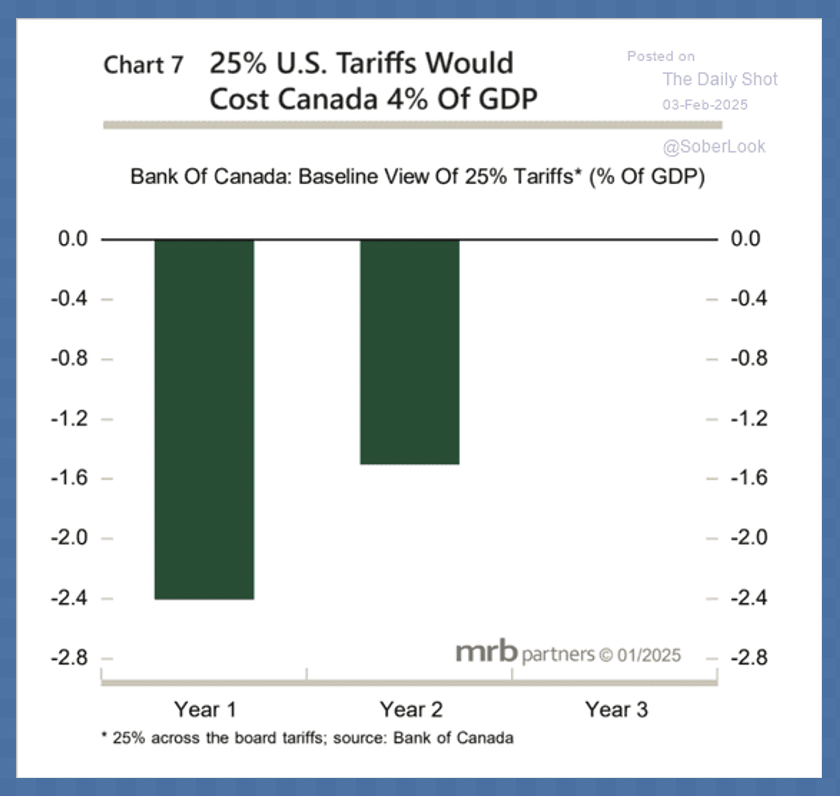

The BoC estimates that real Canadian GDP under a 25% tariff scenario will be a deeply recessionary 4% lower than otherwise (chart below courtesy of The Daily Shot).

The BoC minutes further concluded that the “downward pressure on inflation from weakness in the economy” will likely be so significant that it will counterbalance “the upward pressure on inflation from higher input prices and supply chain disruptions.” In other words, recessions have a reliable history of deflating prices and bringing interest rates down.

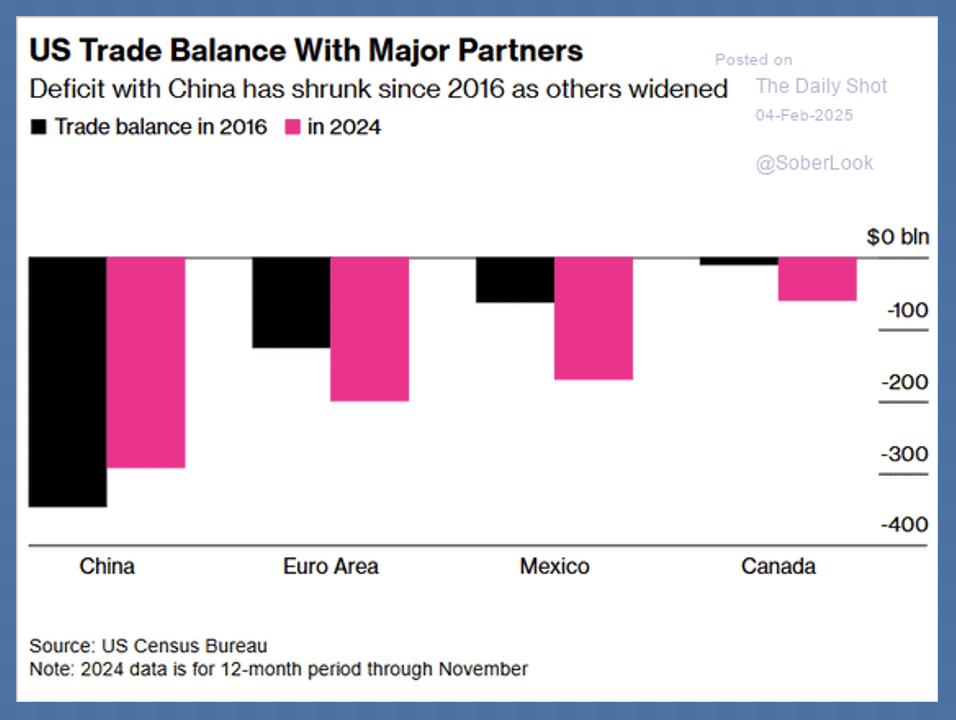

Other countries like China, Mexico, and Europe have larger US trade deficits—exporting more to the US than they import from it (2024 trade deficits shown below in pink, compared with 2016 in black). Tariffs there will exert further drag on the global economy.

Through erratic messaging, it seems that a weak economy is not a bug but the Trump administration’s goal.

The Treasury Borrowing Advisory Committee recommends that short-term Treasury bills (T-bills have terms of less than 1 year) make up 15–20% of total Federal debt. In 2023-2024, 57% of total bond issuance was made up of T-bills, which are currently renewing above 4.25%.

New Treasury Secretary Scott Bessent has said he is focused on extending the term of the $36 trillion in Federal debt to lower interest costs and extend payback periods. For that to happen, Bessent needs the bond market to believe that inflation is under control and that lower interest rates are sufficient compensation for lenders.

Without falling demand and higher unemployment, the cost of living is unlikely to decline enough for the Fed to lower short-term policy rates and, more importantly, for the bond market to lower longer-term fixed borrowing rates.

Oil prices have cooperated, with crude (WTI) deflating to a 52-week low today at sub-$66 a barrel and -8% year over year. Canada’s oil (Western Canadian Select) is sub-$56 a barrel and -15% since Trump’s second inauguration. That’s disinflationary, too.

In his first term, President Trump measured his popularity by how the stock market was doing. In year one of 2.0, it seems the measuring stick is what Treasury prices are doing. If the economy and stock markets dump early, he will no doubt blame it on Biden and the need to curb fentanyl and then take credit for any economic recovery heading into the mid-terms.

Tariffs and government spending cuts will weigh heavily; it seems that’s by design.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Danielle Park March 5th, 2025

Posted In: Juggling Dynamite