ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 9, 2025 | ‘Quantitative Easing with Chinese Characteristics’: How to Fund an Economic Miracle Ellen Brown

Ellen Brown

China went from one of the poorest countries in the world to global economic powerhouse in a mere four decades. Currently featured in the news is DeepSeek, the free, open source A.I. built by innovative Chinese entrepreneurs which just pricked the massive U.S. A.I. bubble.

Even more impressive, however, is the infrastructure China has built, including 26,000 miles of high speed rail, the world’s largest hydroelectric power station, the longest sea-crossing bridge in the world, 100,000 miles of expressway, the world’s first commercial magnetic levitation train, the world’s largest urban metro network, seven of the world’s 10 busiest ports, and solar and wind power generation accounting for over 35% of global renewable energy capacity. Topping the list is the Belt and Road Initiative, an infrastructure development program involving 140 countries, through which China has invested in ports, railways, highways and energy projects worldwide.

All that takes money. Where did it come from? Numerous funding sources are named in mainstream references, but the one explored here is a rarely mentioned form of quantitative easing — the central bank just “prints the money.” (That’s the term often used, though printing presses aren’t necessarily involved.)

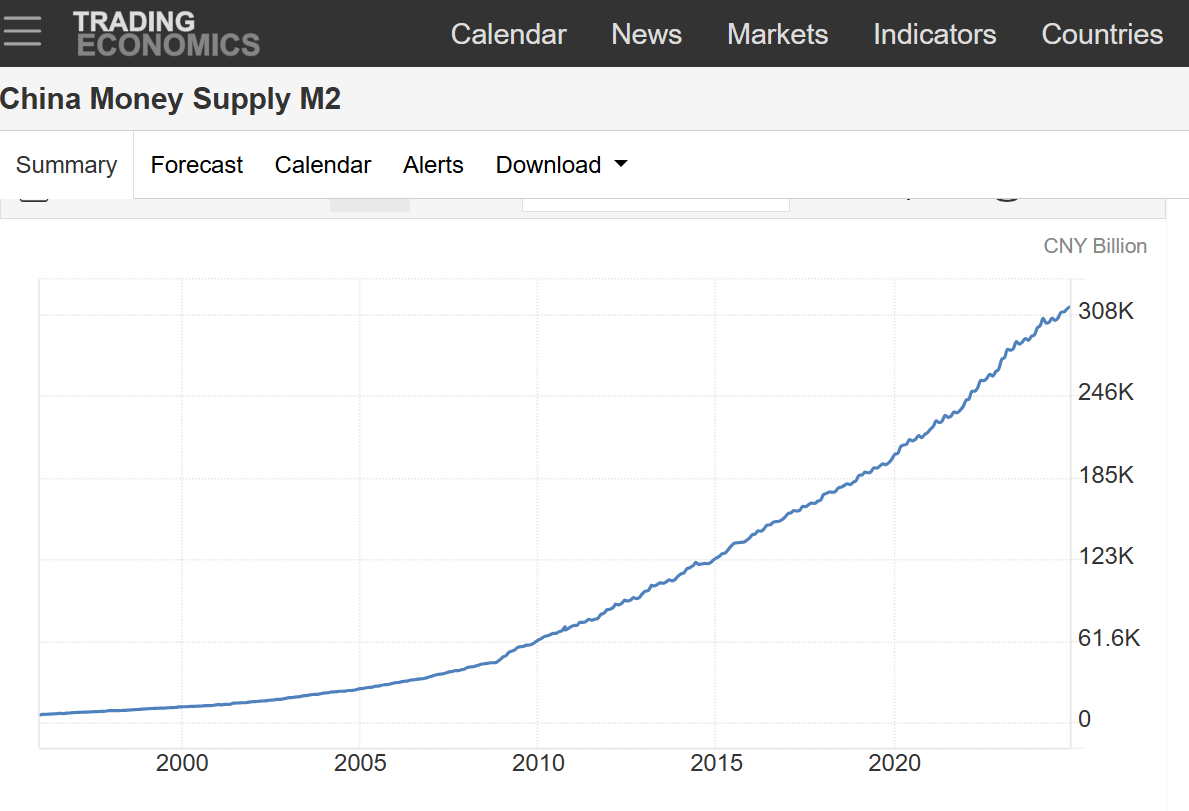

From 1996 to 2024, the Chinese national money supply increased by a factor of more than 53 or 5300% — from 5.84 billion to 314 billion Chinese yuan (CNY) [see charts below]. How did that happen? Exporters brought the foreign currencies (largely U.S. dollars) they received for their goods to their local banks and traded them for the CNY needed to pay their workers and suppliers. The central bank —the Public Bank of China or PBOC — printed CNY and traded them for the foreign currencies, then kept the foreign currencies as reserves, effectively doubling the national export revenue.

Investopedia confirms that policy, stating:

One major task of the Chinese central bank, the PBOC, is to absorb the large inflows of foreign capital from China’s trade surplus. The PBOC purchases foreign currency from exporters and issues that currency in local yuan. The PBOC is free to publish any amount of local currency and have it exchanged for forex. … The PBOC can print yuan as needed …. [Emphasis added.]

Interestingly, that huge 5300% explosion in local CNY did not trigger runaway inflation. In fact China’s consumer inflation rate, which was as high as 24% in 1994, leveled out after that and averaged 2.5% per year from 1996 to 2023.

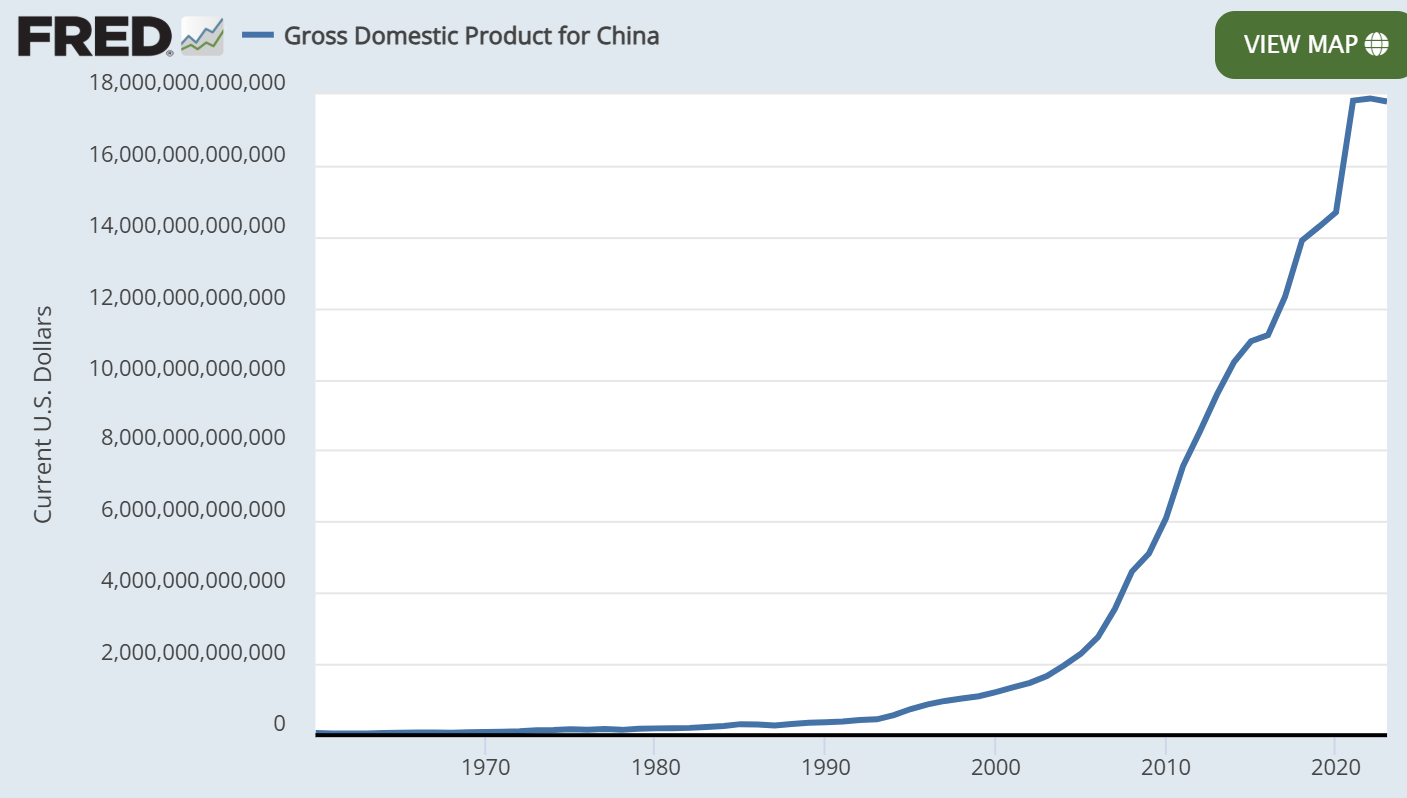

How was that achieved? As in the U.S., the central bank engages in “open market operations” (selling federal securities into the open market, withdrawing excess cash). It also imposes price controls on certain essential commodities. According to a report by Nasdaq, China has implemented price controls on iron ore, copper, corn, grain, meat, eggs and vegetables as part of its 14th five-year plan (2021-2025), to ensure food security for the population. Particularly important in maintaining price stability, however, is that the money has gone into manufacturing, production and infrastructure. GDP (supply) has gone up with demand (money), keeping prices stable. [See charts below.]

The U.S., too, has serious funding problems today, and we have engaged in quantitative easing (QE) before. Could our central bank also issue the dollars we need without triggering the dreaded scourge of hyperinflation? This article will argue that we can. But first some Chinese economic history.

From Rags to Riches in Four Decades

China’s rise from poverty began in 1978, when Deng Xiaoping introduced market-oriented reforms. Farmers were allowed to sell their surplus produce in the market, doors were opened to foreign investors and private businesses and foreign companies were encouraged to grow. By the 1990s, China had become a major exporter of low-cost manufactured goods. Key factors included cheap labor, infrastructure development and World Trade Organization membership in 2001.

Chinese labor is cheaper than in the U.S. largely because the government funds or subsidizes social needs, reducing the operational costs of Chinese companies and improving workforce productivity. The government invests heavily in public transportation infrastructure, including metros, buses and high-speed rail, making them affordable for workers and reducing the costs of getting manufacturers’ products to market.

The government funds education and vocational training programs, ensuring a steady supply of skilled workers, with government-funded technical schools and universities producing millions of graduates annually. Affordable housing programs are provided for workers, particularly in urban areas.

China’s public health care system, while not free, is heavily subsidized by the government. And a public pension system reduces the need for companies to offer private retirement plans. The Chinese government also provides direct subsidies and incentives to key industries, such as technology, renewable energy and manufacturing.

After it joined the WTO, China’s exports grew rapidly, generating large trade surpluses and an influx of foreign currency, allowing the country to accumulate massive foreign exchange reserves. In 2010, China surpassed the U.S. as the world’s largest exporter. In the following decade, it shifted its focus to high-tech industries, and in 2013 the Belt and Road Initiative was launched. The government directed funds through state-owned banks and enterprises, with an emphasis on infrastructure and industrial development.

Funding Exponential Growth

In the early stages of reform, foreign investment was a key source of capital. Export earnings then generated significant foreign exchange reserves. China’s high savings rate provided a pool of liquidity for investment, and domestic consumption grew. Decentralizing the banking system was also key. According to a lecture by U.K. Prof. Richard Werner:

Deng Xiaoping started with one mono bank. He realized quickly, scrap that; we’re going to have a lot of banks. He created small banks, community banks, savings banks, credit unions, regional banks, provincial banks. Now China has 4,500 banks. That’s the secret to success. That’s what we have to aim for. Then we can have prosperity for the whole world. Developing countries don’t need foreign money. They just need community banks supporting [local business] to have the money to get the latest technology.

China managed to avoid the worst impacts of the 1997 Asian Financial Crisis. It did not devalue its currency; it maintained strict control over capital flows and the PBOC acted as a lender of last resort, providing liquidity to state-controlled banks when needed.

In the 1990s, however, its four major state banks did suffer massive losses, with non-performing loans totaling more than 20% of their assets. Technically, the banks were bankrupt, but the government did not let them go bust. The non-performing loans were moved on to the balance sheets of four major asset management companies (“bad banks”), and the PBOC injected new capital into the “good banks.”

In a January 2024 article titled “The Chinese Economy Is Due a Round of Quantitative Easing,” Prof. Li Wei, Director of the China Economy and Sustainable Development Center, wrote of this policy, “The central bank directly intervened in the economy by creating money. Seen this way, unconventional financing is nothing less than Chinese-style quantitative easing.”

In an August 2024 article titled “China’s 100-billion-yuan Question: Does Rare Government Bond Purchase Alter Policy Course?,” Sylvia Ma wrote of China’s forays into QE:

Purchasing government bonds in the secondary market is allowed under Chinese law, but the central bank is forbidden to subscribe to bonds directly issued by the finance ministry. [Note that this is also true of the U.S. Fed.] Such purchases from traders were tried on a small scale 20 years ago.

However, the monetary authority resorted more to printing money equivalent to soaring foreign exchange reserves from 2001, as the country saw a robust increase in trade surplus following its accession to the World Trade Organization. [Emphasis added.]

This is the covert policy of printing CNY and trading this national currency for the foreign currencies (mostly U.S. dollars) received from exporters.

What does the PBOC do with the dollars? It holds a significant portion as foreign exchange reserves, to stabilize the CNY and manage currency fluctuations; it invests in U.S. Treasury bonds and other dollar-denominated assets to earn a return; and it uses U.S. dollars to facilitate international trade deals, many of which are conducted in dollars.

The PBOC also periodically injects capital into the three “policy banks” through which the federal government implements its five-year plans. These are China Development Bank, the Export-Import Bank of China, and the Agricultural Development Bank of China, which provide loans and financing for domestic infrastructure and services as well as for the Belt and Road Initiative. A January 2024 Bloomberg article titled “China Injects $50 Billion Into Policy Banks in Financing Push” notes that the policy banks “are driven by government priorities more than profits,” and that some economists have called the PBOC funding injections “helicopter money” or “Chinese-style quantitative easing.”

Prof. Li argues that with the current insolvency of major real estate developers and the rise in local government debt, China should engage in this overt form of QE today. Other commentators agree, and the government appears to be moving in that direction. Prof. Li writes:

As long as it does not trigger inflation, quantitative easing can quickly and without limit generate sufficient liquidity to resolve debt issues and pump confidence into the market.…

Quantitative easing should be the core of China’s macroeconomic policy, with more than 80% of funds coming from QE…

As the central bank is the only institution in China with the power to create money, it has the ability to create a stable environment for economic growth. [Emphasis added.]

Eighty-percent funding just from money-printing sounds pretty radical, but China’s macroeconomic policy is determined by five-year plans designed to serve the public and the economy, and the policy banks funding the plans are publicly-owned. That means profits are returned to the public purse, avoiding the sort of private financialization and speculative exploitation resulting when the U.S. Fed engaged in QE to bail out the banks after the 2007-08 banking crisis.

The U.S. Too Could Use Another Round of QE — and Some Public Policy Banks

There is no law against governments or their central banks just printing the national currency without borrowing it first. The U.S. Federal Reserve has done it, Abraham Lincoln’s Treasury did it, and it is probably the only way out of our current federal debt crisis. As Prof. Li observes, we can do it “without limit” so long as it does not trigger inflation.

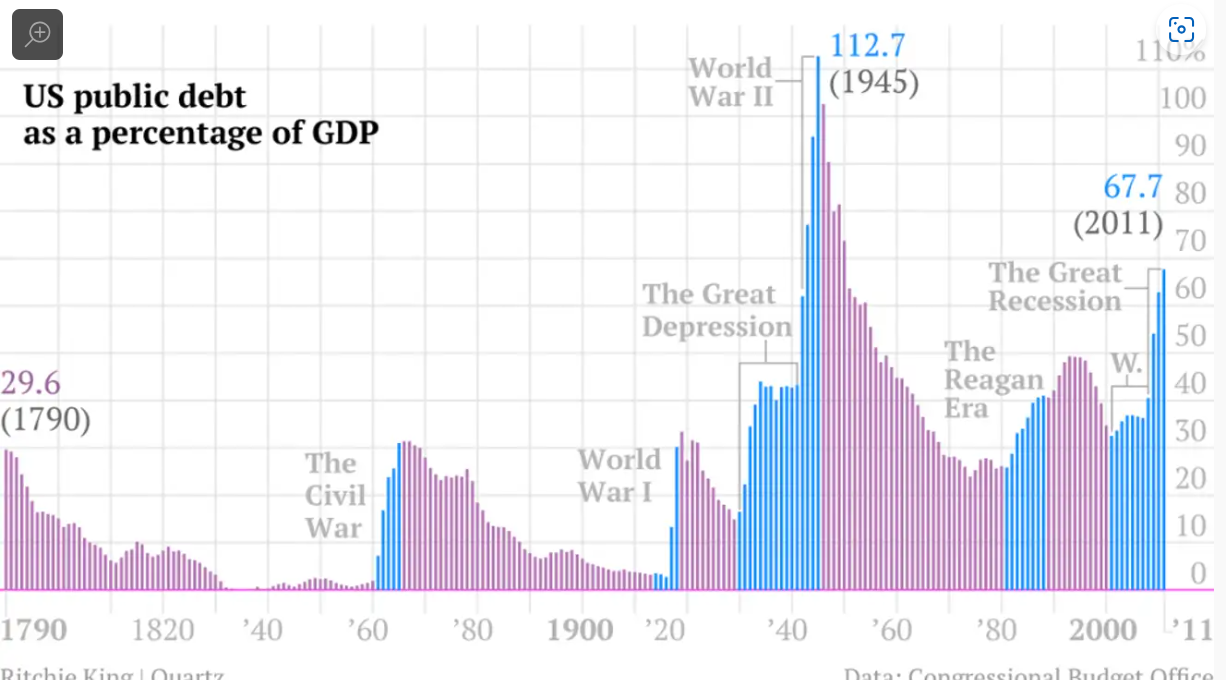

Financial commentator Alex Krainer observes that the total U.S. debt, public and private, comes to more than $101 trillion (citing the St. Louis Fed’s graph titled “All Sectors; Debt Securities and Loans”). But the monetary base — the reserves available to pay that debt — is only $5.6 trillion. That means the debt is 18 times the monetary base. The U.S. economy holds far fewer dollars than we need for economic stability.

The dollar shortfall can be filled debt- and interest-free by the U.S. Treasury, just by printing dollars as Lincoln’s Treasury did (or by issuing them digitally). It can also be done by the Fed, which “monetizes” federal securities by buying them with reserves it issues on its books, then returns the interest to the Treasury and after deducting its costs. If the newly-issued dollars are used for productive purposes, supply will go up with demand, and prices should remain stable.

Note that even social services, which don’t directly produce revenue, can be considered “productive” in that they support the “human capital” necessary for production. Workers need to be healthy and well educated in order to build competitively and well, and the government needs to supplement the social costs borne by companies if they are to compete with China’s subsidized businesses.

Parameters would obviously need to be imposed to circumscribe Congress’s ability to spend “without limit,” backed by a compliant Treasury or Fed. An immediate need is for full transparency in budgeted expenditures. The Pentagon, for example, spends nearly $1 trillion of our taxpayer money annually and has never passed a clean audit, as required by law.

We Sorely Need an Infrastructure Bank

The U.S. is one of the few developed countries without an infrastructure bank. Ironically, it was Alexander Hamilton, the first U.S. Treasury secretary, who developed the model. Winning freedom from Great Britain left the young country with what appeared to be an unpayable debt. Hamilton traded the debt and a percentage of gold for non-voting shares in the First U.S. Bank, paying a 6% dividend. This capital was then leveraged many times over into credit to be used specifically for infrastructure and development. Based on the same model, the Second U.S. Bank funded the vibrant economic activity of the first decades of the United States.

In the 1930s, Roosevelt’s government pulled the country out of the Great Depression by repurposing a federal agency called the Reconstruction Finance Corporation (RFC) into a lending machine for development on the Hamiltonian model. Formed under the Hoover administration, the RFC was not actually an infrastructure bank but it acted like one. Like China Development Bank, it obtained its liquidity by issuing bonds.

The primary purchaser of RFC bonds was the federal government, driving up the federal debt; but the debt to GDP ratio evened out over the next four decades, due to the dramatic increase in productivity generated by the RFC’s funding of the New Deal and World War II. That was also true of the federal debt after the American Revolution and the Civil War.

A pending bill for an infrastructure bank on the Hamiltonian model is HR 4052, The National Infrastructure Bank Act of 2023, which ended 2024 with 48 sponsors and was endorsed by dozens of legislatures, local councils, and organizations. Like the First and Second U.S. Banks, it is intended to be a depository bank capitalized with existing federal securities held by the private sector, for which the bank will pay an additional 2% over the interest paid by the government. The bank will then leverage this capital into roughly 10 times its value in loans, as all depository banks are entitled to do. The bill proposes to fund $5 trillion in infrastructure capitalized over a 10-year period with $500 billion in federal securities exchanged for preferred (non-voting) stock in the bank. Like the RFC, the bank will be a source of off-budget financing, adding no new costs to the federal budget. (For more information, see https://www.nibcoalition.com/.)

Growing Our Way Out of Debt

Rather than trying to kneecap our competitors with sanctions and tariffs, we can grow our way to prosperity by turning on the engines of production. Far more can be achieved through cooperation than through economic warfare. DeepSeek set the tone with its free, open source model. Rather than a heavily guarded secret, its source code is freely available to be shared and built upon by entrepreneurs around the world.

We can pull off our own economic miracle, funded with newly issued dollars backed by the full faith and credit of the government and the people. Contrary to popular belief, “full faith and credit” is valuable collateral, something even Bitcoin and gold do not have. It means the currency will be accepted everywhere – not just at the bank or the coin dealer’s but at the grocer’s and the gas station. If the government directs newly created dollars into new goods and services, supply will grow along with demand and the currency should retain its value. The government can print, pay for workers and materials, and produce its way into an economic renaissance.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Ellen Brown February 9th, 2025

Posted In: Web of Debt