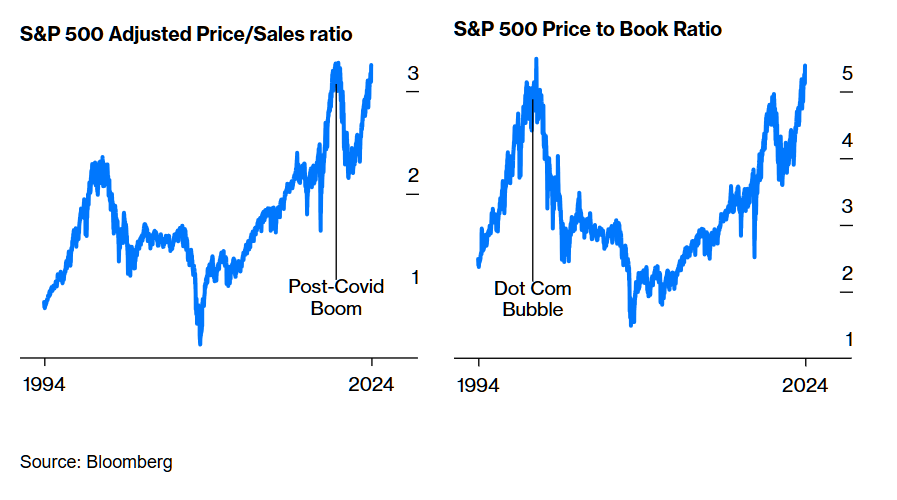

With a price of more than 5x book value (lower right), U.S. stocks are the most overvalued since the tech-mania top in March 2020. At 3x price-to-sales (lower left), the recent euphoria has returned to the fall 2021 level and significantly overshot the 2000 top.

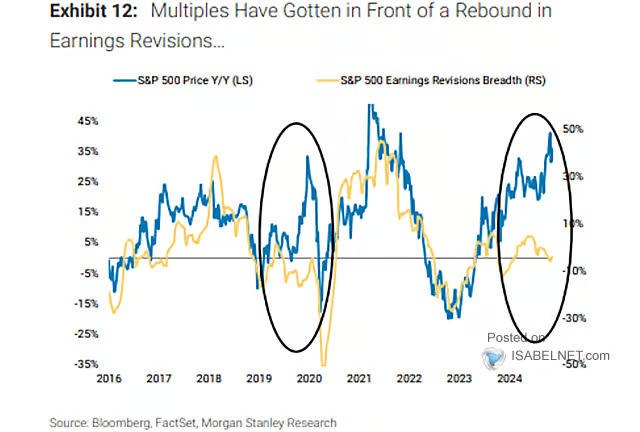

As the S&P 500 has rebounded sharply over the past year (blue line below since 2016, courtesy of Isabelnet.com), earnings estimates (yellow line) have moved in the opposite direction. The extreme disconnect between earnings estimates and prices (circled below on the far right) is unusual. A lesser overshoot of prices in late 2019 (circle on the left) resolved with stock prices collapsing into spring 2020.

As the S&P 500 has rebounded sharply over the past year (blue line below since 2016, courtesy of Isabelnet.com), earnings estimates (yellow line) have moved in the opposite direction. The extreme disconnect between earnings estimates and prices (circled below on the far right) is unusual. A lesser overshoot of prices in late 2019 (circle on the left) resolved with stock prices collapsing into spring 2020.

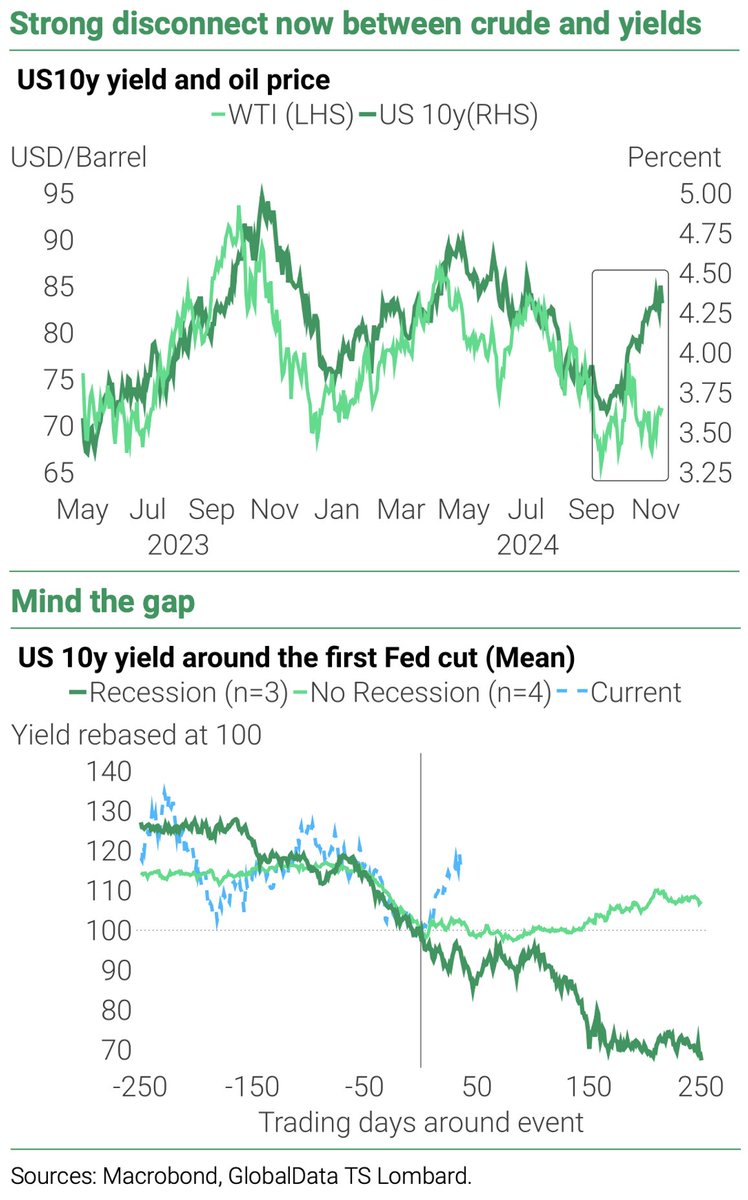

A similar disconnect is evident today between the price of oil (WTIC below in light green since May 2023) and the U.S. 10-year treasury yield (dark green), where oil prices have continued to slump (disinflationary) even as Treasury yields have rebounded since September.

Treasury yields typically back up first (on inflation expectations) and then fall during Fed cutting cycles as the economy weakens. However, since the Federal Reserve’s first rate cut on September 18, the degree of backup in yields has been larger than average (blue shown above in the lower panel versus past recessionary periods in dark green and rare soft-landings in light green).

Yields could back up further while investors believe that Trump’s policies might revive inflation. But for how long? The plan to slash government spending (which drives some 35% of the U.S. economy today), increase unemployment and boost oil production should all be disinflationary.

Higher yields/rates are ultimately self-correcting because they serve as a tourniquet on credit growth through the banking system. We already see higher mortgage and commercial credit rates in collapsing loan applications. That makes sense.