ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

September 1, 2024 | Your Portfolio and the Election

John Mauldin

Labor Day weekend finds me in far northwest British Columbia, fishing with 29 of my readers. The conversations are deep and fascinating, and it should be no surprise that politics and markets are brought up more often than not. Labor Day is traditionally when most Americans, other than us political junkies, actually begin noticing politics.

I asked my great friend and business partner David Bahnsen, who is about as politically wired as anyone and one of the truly great economic and investment minds, to reflect on the intersection of politics and markets. It is a quick, balanced, and reasonable read—which is why I assigned him the project rather than doing it myself. Besides, he does a better job than I could. So let’s jump in.

Your Portfolio and the Election by David Bahnsen

We are officially in that season when investors begin obsessing over the presidential election, joining the media’s excessive interest in something highly unlikely to have the impact they expect. This isn’t to say elections don’t matter. They do. In matters of personal preference, policy convictions, civic and cultural vision, and yes, market and economic impact, elections can make a difference. My comment is about magnitude.

Elections tend to be overrated in how much they can improve an individual’s life, the conditions one cares about in the country, and yes, the markets and economy. But having a more modest view of impact is not the same as advocating for total apathy. Elections matter, and complacency is anti-patriotic and anti-democratic.

The specific political calculus is different every four years (really, every two years, for those taking a close enough interest), and contextualizing our analysis of the election and its expected impact on investors requires a deeper dive.

Can’t We All Get Along?

You may have noticed how politics has become a loaded and often toxic part of American public life. To an extent this has always been true—politics has had the potential to be a divisive topic for decades. But objectively, it seems and feels worse now than it has in my lifetime. Friendly discourse is hard to come by, and “mere political disagreement” is rare. The stakes have been elevated to threaten friendships, workplaces, and even families.

The “us vs. them” tribalism overtaking American politics is a tragedy not only for its impact on social cohesion, but also for the diminished intellectual contemplation it creates. Constructing cogent public policy is much harder when one is forced into a box “their side” would approve of, and especially if one believes any opposition to their policy proposals means the opposing side is “evil.” This has all gone out of control, but I would be wrong to say I thought it was about to get better. Sadly, a deep divide has taken hold, and I suspect we are years away from it improving.

I bring all that up because I want to make clear that I am not writing about politics in John Mauldin’s Thoughts from the Frontline because I have a political or partisan agenda to share. My aim herein is for the betterment of investors. There are considerations investors may want to remember in this election season and potential consequences that are fair game in any objective sense. But in the spirit of civility, fair play, and transparency that I lament as missing in the preceding paragraph, some disclosures may be useful before we begin.

I am a center-right movement conservative. I have been since kindergarten when I began reading Bill Buckley and National Review. I am a strong advocate of free enterprise, and I generally favor a constrained vision for the state’s role in the marketplace. I would love to tell you my analysis is devoid of any bias or presuppositions, but I don’t believe that is possible.

There ought to be a clear distinction between one’s description of “what is” and their prescription for “what ought to be.” When it comes to investment advice, I meticulously strive for exactly that (and even consider it my fiduciary duty to do just that!). But I just feel John’s readers deserve to see my cards on the table. Here they are.

- I have never voted for a Democrat for president, and I won’t be this year, either.

- I also didn’t vote for the Republican nominee the last two elections, and I won’t be this year, either.

- I was registered as a Republican from age 18 to age 49 and am now registered Independent.

My partisan allegiances are more flexible these days, but my ideological leanings are as pronounced as ever—I believe in the American experiment, a limited federal government, fiscal sanity, and a populace rooted in self-government and individual responsibility. Dare to dream.

I bring this up to make abundantly clear that no offense is intended by anything I say. I am who I am, and I call balls and strikes out of that reality.

Predicting the Unpredictable

The first thing to be said in assessing this election cycle is that we live in crazy times. It was late June when that fateful debate doomed President Biden’s prospects, and the next several weeks saw years of history unfold. It is hard to believe that an assassination attempt on former President Trump, unsuccessful by mere centimeters, is not even remembered anymore. That story alone is one for the history books, but the story of the Democrats not having a primary season, seeing an incumbent President withdraw his own candidacy for the first time since 1968, and the way in which the party coalesced around the Vice President as their candidate all speak to the rapidity with which things change.

The idea that someone on Labor Day weekend believes they know the result over two months out is insane. The last two presidential elections were determined by less than 80,000 votes, combined, in just a few states, out of 150 million votes cast. We are in a 50–50 country in so many ways, and the nature of the electoral college makes it very difficult for either candidate to run up the score in the states where they are most popular. The reasonably high floor of both candidates (45–46% by my analysis), but also the reasonably low ceiling of both candidates, makes this an election that will most likely, once again, be settled by thin margins in just a handful of states (and within those, by just a handful of counties).

It also is not true that investors would gain a significant edge in markets if they knew who the next president were going to be. Whoever occupies the White House has a certain amount of executive authority, strong discretion in the appointment of judges, the ability to veto legislation (as if that happens much), and a lot of leeway over personnel in cabinet departments. Yet the separation of powers embedded in our Constitution doesn’t allow the president carte blanche in passing legislation.

The bicameral nature of our legislature means that both the House of Representatives and the Senate are needed for legislation to pass. In fact, one of the most underreported realities of the Biden administration is that with a numerical majority in the US Senate and House they were unable to pass their signature and most ambitious legislative project (the so-called Build Back Better Act). While the Democrats [narrowly] lost their majority in the House in the 2022 midterms, they had a majority of the Senate all four years, and in 2021 were blocked from passing Build Back Better by members of their own party (Senators Manchin and Sinema from West Virginia and Arizona, respectively). In other words, not only do presidents often need bipartisan support to pass legislation, but they are also not even assured a blank check with their own parties.

I do not make my living projecting what Nvidia stock will do next and I certainly don’t make my living doing political prognostication. I stand by my earlier call on the presidential race—it is a 50/50 country and the odds for each candidate should be considered something in the range of 50/50. An argument can be made for why Kamala Harris has a certain momentum and the advantages that come with her opponent’s liabilities, but an argument can also be made that the electoral college gives Donald Trump an embedded edge, along with the challenges the incumbent party has around immigration and inflation. It is going to be a wild two months, and I do not mean that as a positive thing.

Historical Context

I will soon get to my analysis of what these particular candidates may or may not represent when it comes to economic outlook and market opportunity. But let’s first just understand why associating a market outlook with a partisan aspiration is so futile.

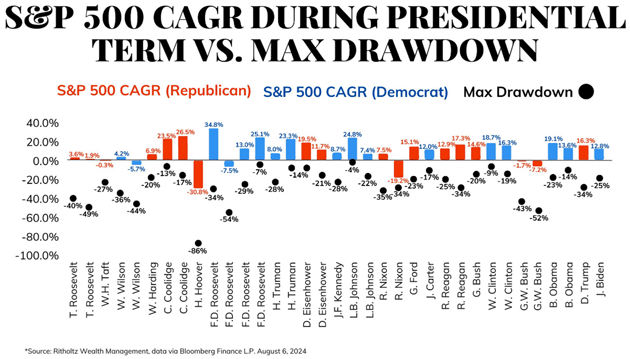

Here is a little secret: Markets have generally gone up under Republican presidents and markets have generally gone up under Democratic presidents, and the reason for that is… wait for it… markets just generally go up.

Put differently, the profit motive doesn’t take a nap when a new president is inaugurated, and American companies have a remarkable way of staying laser-focused on maximizing profits no matter who is in the Oval Office.

Source: David Bahnsen

You are welcome to believe Herbert Hoover uniquely ushered in the Great Depression, or that George W. Bush particularly created the Global Financial Crisis of 2008. But what you basically see throughout 125 years of modern history is that the average drawdowns are similar under presidents from both parties, and the compounded annual growth rate is virtually identical. The narrative that has not worked is this:

My Republican friends: “President Obama is an enemy of markets and free enterprise and he is going to tank the economy for investors.” WRONG: The stock market was up eight out of eight years when he was president.

My Democrat friends: “President Trump is an enemy of norms and institutions, and his erratic ways are going to tank the economy for investors.” WRONG: The stock market was up 70% in his Presidency, despite the global COVID pandemic and shutdown.

These are the most recent examples of strong partisan angst being applied to expectations for markets, and markets having no interest in cooperating. But let’s dig a little deeper. Was President Reagan a good president for markets? I would argue so (remember my prior confession). Huge efforts at deregulation and marginal tax relief could not have hurt. There was surely some cause and effect. But were the 1980s likely to be a period of great growth in corporate profits, regardless? It’s certainly possible.

Was President Clinton a good president for markets? I would argue so (see, I am objective!). But was his presidency really the prime driver of the huge technology boom that ensued the second half of the 1990s? Of course not. Timing is everything, at least for how history remembers presidents.

Was President George W. Bush a disaster for markets? Well, the market actually went up +100% in the middle of his presidency (from Oct. 2002 through August 2007). But if you are bookended by a 40% drop at the beginning of your presidency and a 50% drop at the end (the dot-com crash to start and the Global Financial Crisis to end), it is going to be hard to see a strong result.

Was Barack Obama a good president for markets? On one hand, the market was up every year of his presidency; on the other hand, he took over at a generational bottom in the midst of a depression-type recession with a trough in earnings, and then an unprecedented era of monetary accommodation (an entire presidency with a 0% fed funds rate, and $4 trillion of quantitative easing!).

Your assessment of certain presidents may impact your opinions as to how they aided or hurt markets, but in almost every case there are objective arguments to be made for both. Timing matters. Circumstances matter. Luck matters. The Fed matters. And yes, presidential policy matters. But you know what doesn’t seem to matter? Party affiliation.

I don’t make up the facts; I just report them.

Likewise, the tax bill that passed in late 2017 (effective for 2018) contained a lot of bells and whistles investors predictably loved. From significantly lower corporate income tax rates to repatriation of foreign profits to a doubling of the estate tax exclusion amount to opportunity zones, there were plenty of components that investors naturally appreciated.

The 2018 market volatility, though, centered around the uncertainty of Fed policy (not under the president’s control) and the uncertainty of Trump’s tariff/China policies. If all we know is that one candidate wanted somewhat lower tax rates and the other didn’t, we don’t really know enough to know the expected market impact. First of all, the political realism of the policies matters (which is why markets never respond to crazy, onerous tax ideas like taxing unrealized gains—because the market rightly believes it is just politicians blowing air). Further, there is more to an economic agenda than just tax policy. I would argue that much of the favorable market conditions in President Trump’s term were more about deregulation than improved corporate tax rates. Energy policy matters. Trade policy matters. Personnel matters. There is a lot to an economic policy portfolio.

And this leads me to my underlying point about how investors ought to discount the two presidential possibilities we now face: How does one discount what they do not know? Thus far Kamala Harris has stated that her economic agenda is to give the FTC the ability to implement price controls on grocery stores (good luck with that), to give first-time home buyers $25,000 to help with their down payment, to implement a $6,000 child tax credit, and to stop taxing tips on service workers. Donald Trump said each of the latter two points before she did and has also said he will “make it the greatest economy you have ever seen.” And I will not lie—the “greatest economy we have ever seen” sounds like a good deal to me, but I am not totally sure how he plans to do that.

Trump has talked about high tariffs on imported goods, but also talked about only threatening to do so as a bargaining chip. He has not said much about tax rates at all. He has generally alluded to deregulation but has not been forthcoming on where he would deregulate. It is reasonable to believe he would be pushing for more energy approvals (drilling, pipelines, projects, etc.). But really, neither candidate is being specific on their policy ideas.

The Elephant in the Room

From tax policy to regulation to energy, the contrast between the two candidates is stark. Contrasts are easy to draw, even if the magnitude of impact is not.

However, the one area where it is safe to assume things will not get immediately better with either candidate is government spending and the government debt that supports the spending.

The national debt was $19 trillion when former President Trump took office, and it was $28 trillion when he left office. Vice President Harris has seen it increase another $7 trillion. Peace time, war time, good economy, bad economy, health scare, no health scare—it is the most bipartisan thing in America: Government spending keeps growing.

As John has documented, from entitlement spending to debt-to-GDP ratios to absolute levels of debt, we have unsustainable dynamics that are screaming for solutions. Some solutions exist, but none that are pain-free. Regardless, no such solutions are on the ballot in 2024. No one is running on Social Security solvency. No one is running on a balanced budget. No one is running on fiscal sanity.

This speaks to the reality of this election: There are some differences on various policy categories that matter (tax, regulation, trade, energy) if you assume certain things about both candidates; but when it comes to the most significant economic issue of our generation—the government debt level—there is nothing encouraging on the table.

Conclusion

I have gone on longer than I intended to so I will hold for a future Dividend Café additional commentary on health care, drug pricing, the impact of tariffs, and expectations around personnel (i.e., new Fed governors, anyone?).

My closing caution to you is to not settle for superficial analysis. I use as an example the following: I have said in this paper that Trump was a solid pro-energy president; energy was the worst-performing sector in his administration. He spent much of his time in office fighting with big tech; technology was the best-performing sector during his term in office.

Conversely, President Biden declared war on energy upon coming into office, cancelling the Keystone Pipeline, denying new permits on federal land, and eventually halting new opportunities for LNG export. Yet energy has been the best-performing sector during his term in office.

This is more than just anecdotal trivia. Markets and politics mix a lot less than we think, and they mix a lot differently than we expect. When you take an election cycle as crazy as this one has already been, add in the lack of policy specificity, consider the high likelihood of some form of divided government next year, and the low correlation between apparent policy biases and market reality, this election is not yet actionable when it comes to one’s portfolio positioning.

This can all change. More will be revealed in the weeks and months to come. The Fed is set to begin cutting rates. We will get more economic data. And when all is said and done, a country with over a 100% debt-to-GDP ratio is going to be there.

I think I’m writing in “dividend growth” on my ballot.

Dallas and Birthdays

Source: John Mauldin

I will be in Dallas for a few intense days in the middle of September meeting with Mike Roizen and our team as we finalize the launch of our new longevity business project. Then back to Dorado Beach preparing for my 75th birthday with a lot of family and some friends.

I have not really touched my book for the last two weeks, but starting Tuesday I will be in an intense sprint to finish it by October 3, except for 4–5 pages that I will write immediately after the election. Like David, no matter who wins, I think we are on a path for significantly increased debt and moving closer to that final crisis, where the bond market literally throws a tantrum, and we see a global crisis as the world’s reserve currency struggles.

Let me make a prediction: The 2028 election will finally talk about deficits and debts, but absent a true crisis, there will be no real substance beyond vague proposals to tax the rich or cut spending. Concrete choices will be too painful. Sadly, in 2028 we will all agree that deficits and the ever-increasing debt is really, really, really bad but we won’t agree on solutions, as a true solution will involve compromise. Sigh.

But life will go on, we will Muddle Through, perhaps with a few more bruises, and once the crisis is resolved to the bond market’s satisfaction, the future will be better than ever. The trick for us who are a little bit older is to make sure that we get through that period to enjoy those future halcyon days.

With that, it is time to hit the send button. I hope you can spend your weekend and Labor Day with family, friends, and great conversations like I am. Have a great week!

Your wondering how I got to be 75 years old analyst,

John Mauldin

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

John Mauldin September 1st, 2024

Posted In: Thoughts from the Front Line