ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 14, 2024 | The Canadian Housing Bubble Needs To Burst

Hilliard MacBeth

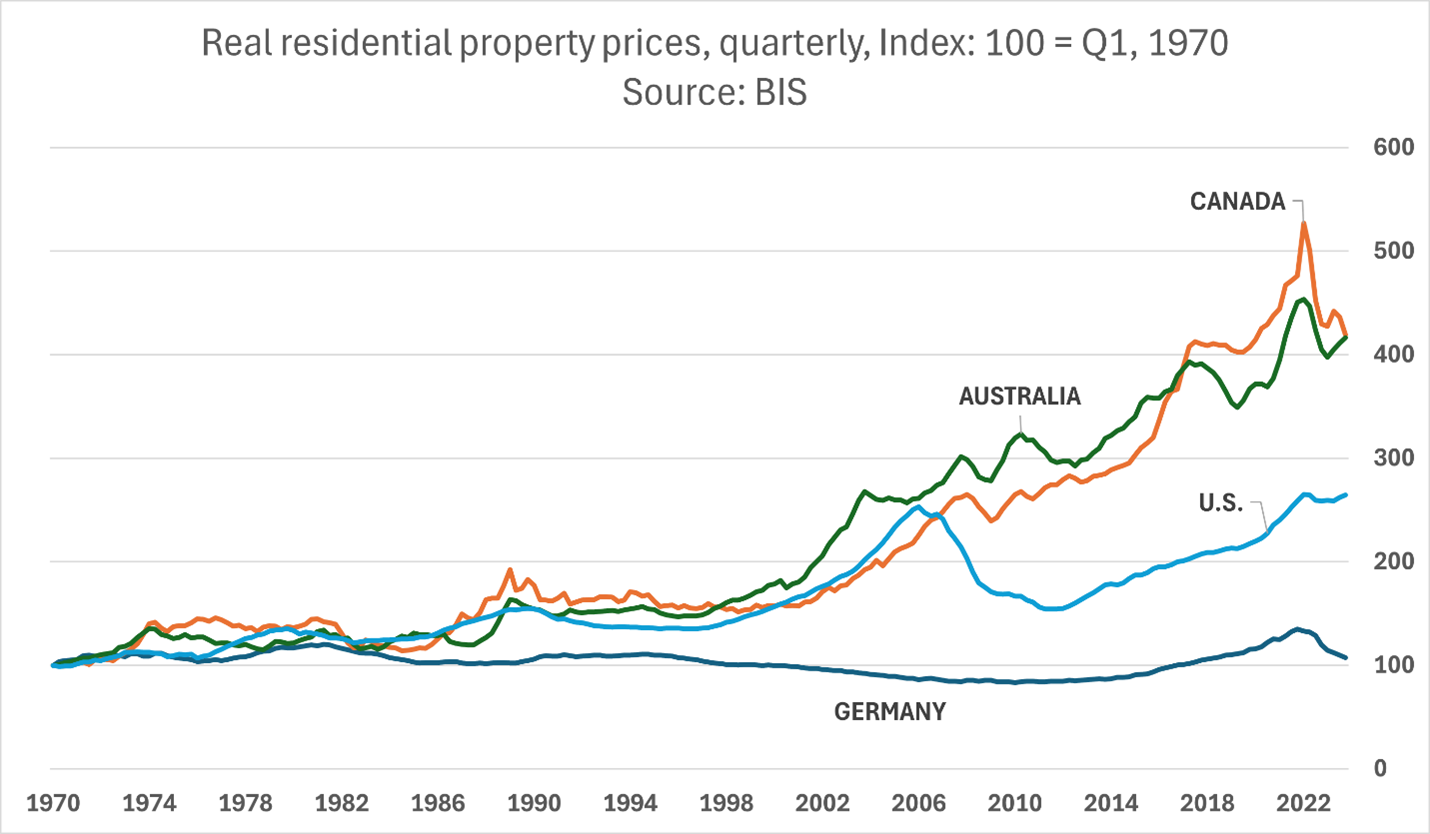

Real residential house prices in Canada have grown by more than four-fold since 1970. This means that house prices have grown much faster than inflation, and housing unaffordability is extreme compared to the past and other countries like the U.S.

Can the housing market in Canada be fixed?

This chart shows prices indexed to 100 in 1970 up to the end of 2023, with data from the Bank for International Settlements (BIS). This index has been deflated by the rate of inflation. The recent drop in the Canadian index happened when inflation soared to 7 percent in 2022 and house prices declined.

Source: MacBeth MacLeod Partners, BIS

The chart shows three other countries — the U.S., Germany and Australia. Two of those countries never achieved the levels seen in Canada, although the U.S. tracked Canada’s bubble until 2006 when the sub-prime mortgage meltdown and the Global Financial Crisis knocked 38 percent off prices. And Germany never experienced a bubble due to stricter rules for mortgage lending. As a result only about 40-50 percent of Germans are owners while the remainder live as long-term renters. Australia is similar to Canada.

The Canadian house price bubble continued to grow almost without interruption until recently. In the 1990s there was a long pause in the bubble, but prices were not expensive before then so it was only a modest decline of 25 percent from the peak in 1989 to a bottom in 1998.

For house prices to form a bubble of the size reached in 2022 there had to be a large amount of mortgage credit on generous terms provided to a large number of borrowers. Rising house prices allowed lenders to pretend that these loans were sustainable. And these mortages were bearable for a number of years, as interest rates were kept close to zero from 2010 to 2020. But since rates have increased from below 1 percent on variable mortages to more than 5 percent house prices have started to slide. With higher rates it has become difficult for many households to make their mortgage, auto and credit card payments.

And some households cannot make their payments. For the first time since 2020 Canadian households are starting to miss payments on mortgages. This is significant because people will skip payments on credit cards and auto loans before they miss a mortgage payment.

According to Equifax, as reported in the Toronto Star on June 11, total mortgage balances reaching “severe delinquency” exceeded $1 billion for the first time in Ontario. And Canada-wide, 1.26 million consumers have missed at least one payment on a credit commitment in early 2024.

The house price correction will gain momentum when unemployment soars — it is already at 6.7 percent in Ontario.

Foreclosure action on houses and condos will be the blunt force that pushes prices much lower. So far this has been avoided by mortgage amortization extensions and lender forbearance. But lenders, regulators and governments have run out of ways to delay the inevitable crash.

Hilliard MacBeth

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson Wealth or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results. The comments contained herein are general in nature and are not intended to be, nor should be construed to be, legal or tax advice to any particular individual. Accordingly, individuals should consult their own legal or tax advisors for advice with respect to the tax consequences to them, having regard to their own particular circumstances.. Richardson Wealth is a member of Canadian Investor Protection Fund. Richardson Wealth is a trademark by its respective owners used under license by Richardson Wealth.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Hilliard MacBeth June 14th, 2024

Posted In: Hilliard's Weekend Notebook