ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

February 21, 2024 | Mortgage Rates Rise Back to 7%, Housing Market Re-Freezes, Buyers’ Strike Continues. Prices Are Just Too High

Wolf Richter

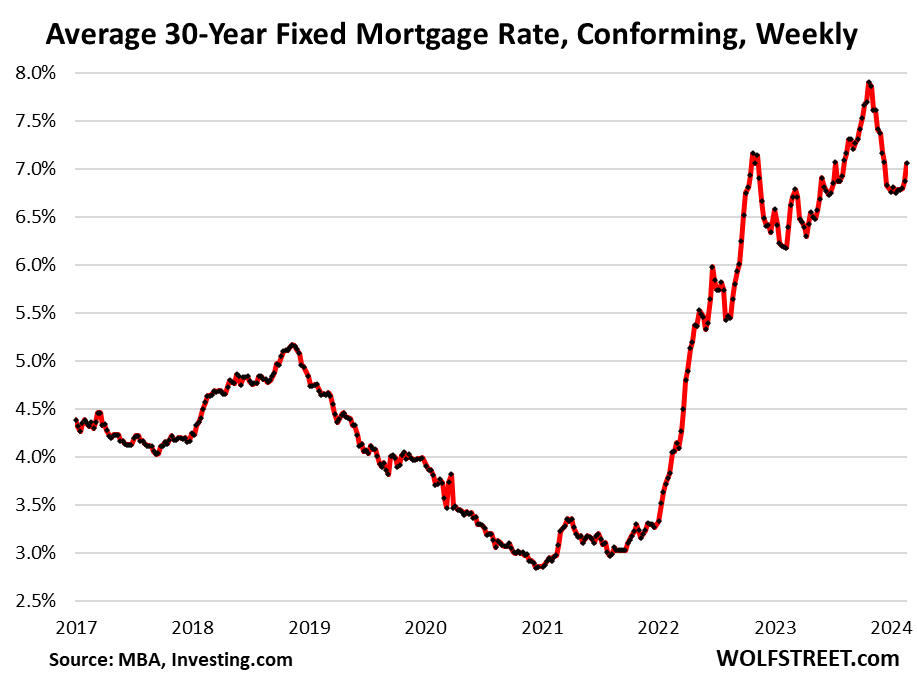

The average conforming 30-year fixed mortgage rate rose to 7.0% in the latest week, according to the Mortgage Bankers Association today. The daily measure by Mortgage News Daily has been over 7% for days. These are the highest rates since mid-December, when they were on their way down.

Mortgage rates had been flirting with 8% back in October last year when the rate-cut mongers fanned out in droves all over the media. Amid enormous hoopla about a gazillion rate cuts in 2024, starting in January, longer-term yields plunged. Mortgage rates plunged with them, with the average 30-year fixed mortgage rate, as tracked by the MBA, falling as low as 6.75% in mid-January. And it was going to be the next boom in the housing market. And then inflation data came in and called for order.

Housing market still frozen.

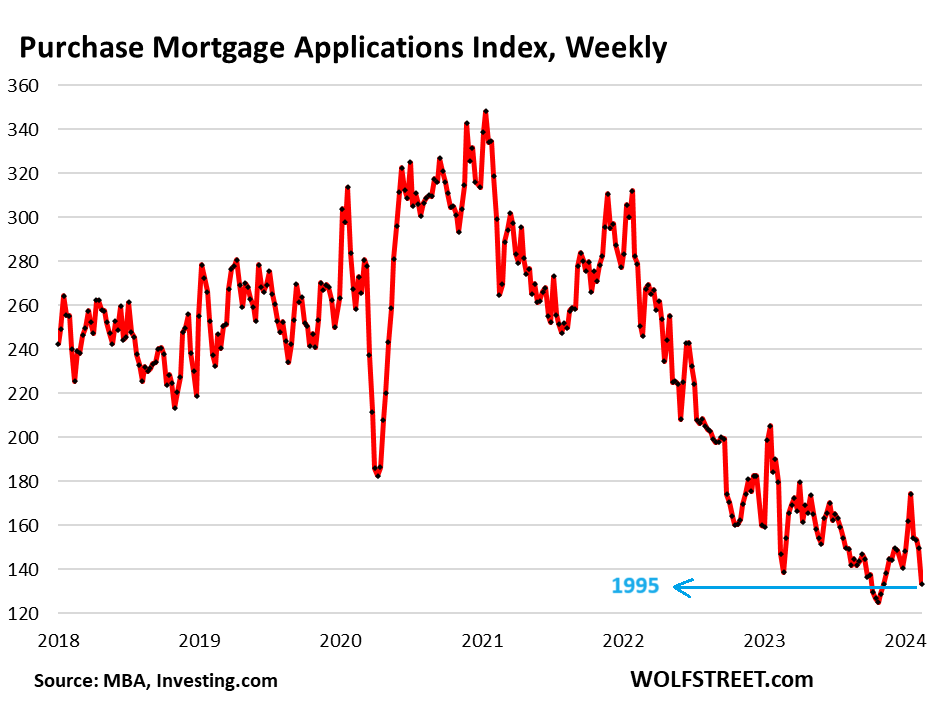

That relatively small increase in mortgage rates caused mortgage applications to re-plunge – after they’d barely risen from the record lows going back to 1995 – a sign that the housing market remains frozen because prices are still too high, and potential sellers are still thinking that this too shall pass, and potential buyers have figured it out.

Mortgage applications to purchase a home plunged by 10% in the latest week from the prior week, seasonally adjusted, according to the MBA.

Mortgage applications were down by 9% from the already depressed levels in the same week a year ago. They were just a hair above the late-October record lows in the data going back to 1995. They’re down by:

- 2022: -47%

- 2021: -42%

- 2019: -43%

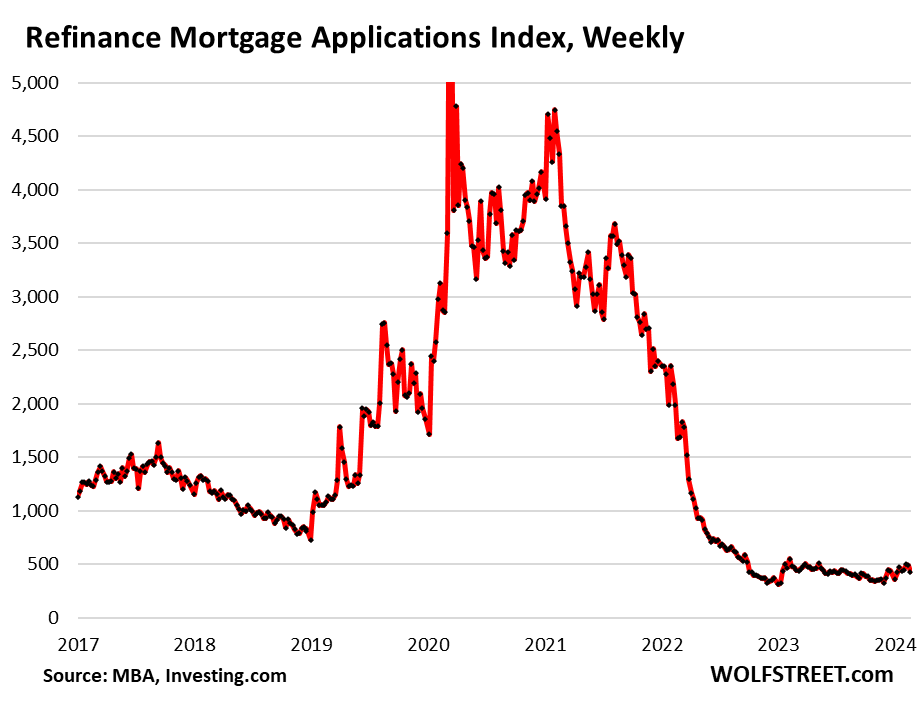

Mortgage applications to refinance a home plunged by 11% from the prior week, but that drop is barely visible amid the collapsed levels since mid-2022. Refinance applications were down by 89% from the same week in 2021:

Buyers’ strike continues.

There is always the issue that the hope of lower mortgage rates is freezing the market further, beyond what the far-too-high prices are already doing.

Inflation doesn’t look like it’s wanting to go back into the bottle voluntarily, but needs to be forced back into the bottle. If prior episodes with this type of inflation are any guidance, this will take years or maybe decades, interrupted by several massive inflation head-fakes where inflation goes down temporarily, leading to rate cuts, only to resurge to even worse levels, leading to even higher rates.

This idea that inflation will be back to 2% and stay there may turn out to be “transitory,” to borrow Powell’s infamous term. And then these higher mortgage rates are going to be with us for years, and maybe for decades, as they had been in past decades.

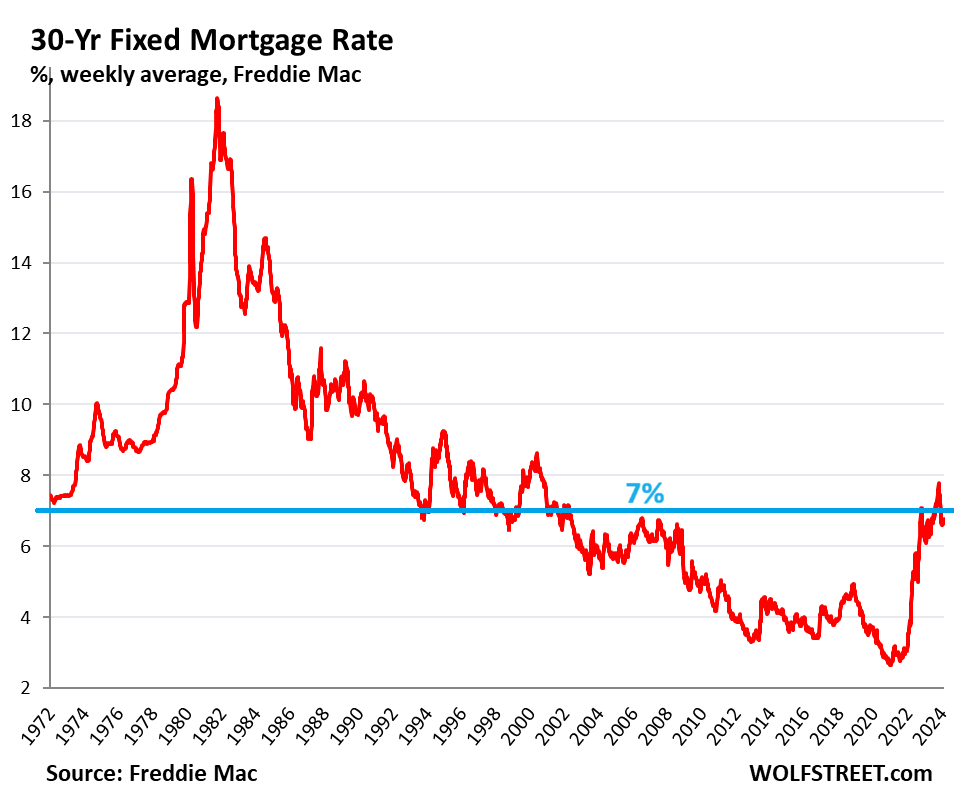

A 7% mortgage rate was considered low – or impossibly low – in the three decades from 1970 through 2000. And homes sold just fine, but at lower prices. Here is the average 30-year fixed, as tracked by Freddie Mac through last week (it will release the new data tomorrow), with the 7% line in blue:

What is over is the frenzied no-questions-asked national mania in 2021 and early 2022, when mostly Millennials – in their peak earnings years – and GenZers were trampling all over each other and knocked each other out, and outbid each other to “nab” that overpriced house, and thereby bid up prices in a historic manner, in order to lock in the low mortgage rates that were beginning to rise as inflation was kicking off.

Now the hope for lower mortgage rates is holding back potential buyers and potential sellers alike – sellers that already bought a home but didn’t put their vacant home on the market because they wanted to ride up the spike all the way. There was a lot of that. Now they’re trying to rent it out, or turn it into a vacation rental, and there’s a lot of that too, but it’s not easy, and the carrying costs of a house are high. So waiting for much lower mortgage rates is lining up to become an expensive bet.

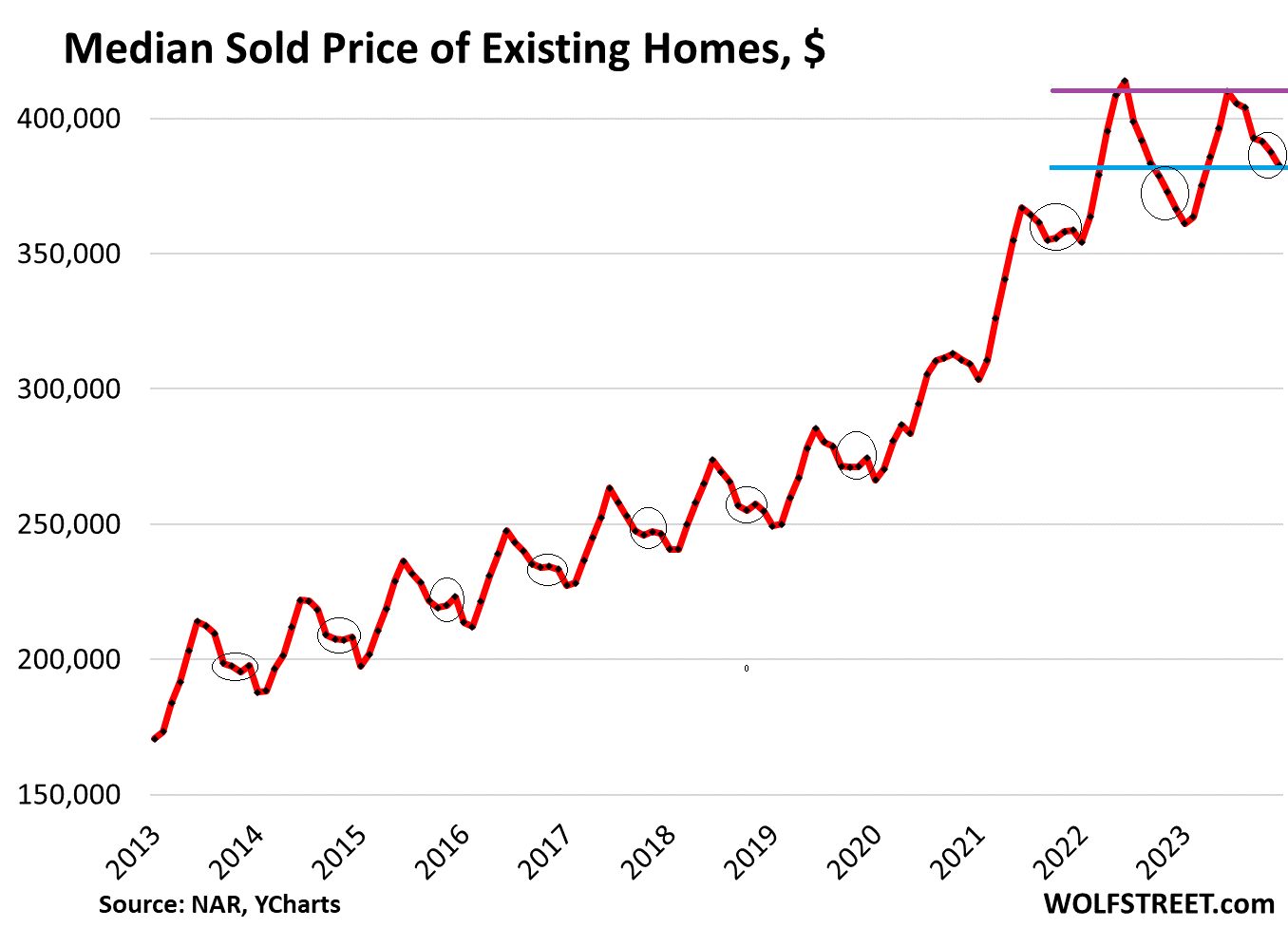

Homebuilders have figured out the drill and kept sales at decent levels by cutting prices, building at lower price points, and buying down mortgage rates. The median price of new houses has dropped 17% from a year earlier to a two year low, not including the costs of the mortgage-rate buydowns, which come out of builders’ profit margins.

But homeowners that want to sell have not figured it out. Sales of existing homes have collapsed. And the national median price has put in a double top, with the high point in June 2022, the first such situation since the housing bust. In some markets prices are still rising, but in others prices are spiraling down, and that’s how it washed out nationally, according to the National Association of Realtors:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter February 21st, 2024

Posted In: Wolf Street