ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

October 18, 2023 | 30-Year Treasury Yield Spikes past 5%, 30-year mortgage rates hit 8%, Mortgage Applications Plunge

Wolf Richter

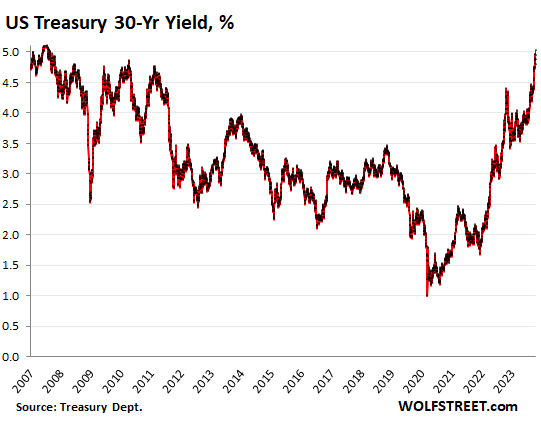

Today it’s the 30-year Treasury yield that pierced the 5% line. It currently trades at 5.02%, the highest since August 2007.

The first of the long-term yields to spike through the 5% line was the unloved 20-year Treasury yield on October 3; it currently trades at 5.25%.

These long-term yields above 5% are an indication that a form of normalcy is gradually being forced upon the bond market by the resurgence of inflation, and by the belated realization that this inflation isn’t just going away on its own somehow. This is a huge regime change, after years of the Fed’s QE and interest rate repression, and all prior assumptions are out the window.

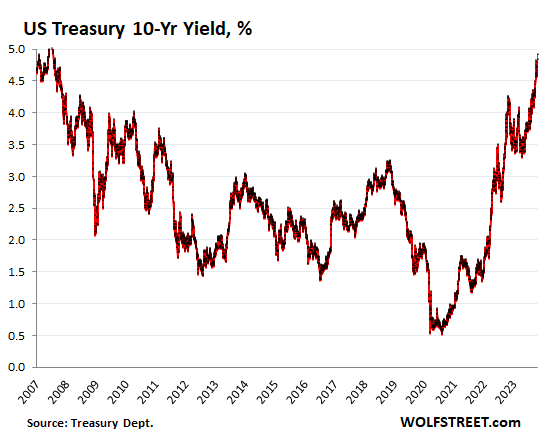

The 10-year yield jumped to 4.92% at the moment, the highest since July 2007, edging within easy reach of the magic 5% line.

Bond market delusions fade.

It seems, the long-term Treasury market is gradually coming out of its delusion about inflation and normalizing interest rates after having spent 18 months believing in the hype about a Fed pivot and rate cuts to something like 0% that would be forced on the Fed by a steep recession, with lots of forever-QE to follow, or whatever.

Instead, consumers are earning lots of money and are spending like drunken sailors. Businesses are spending and investing too. And the government is the biggest drunken sailor of all, further boosting the economy, and throwing more fuel on inflation.

And this deficit-spending by the government has to be funded by piling enormous amounts of Treasury securities on the market that need to find buyers. Yield solves all demand problems by rising until demand emerges. And that’s in part what we’re seeing now.

All of this is happening as the Fed is unloading its balance sheet at record pace, having already shed over $1 trillion in securities in a little over a year.

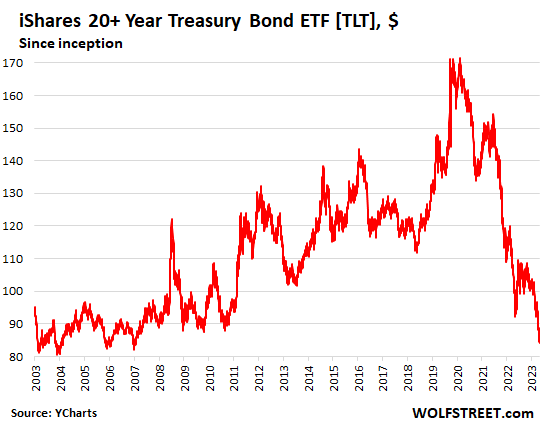

Bond bloodbath for investors that bought during QE and still hold this stuff.

Higher yields mean lower prices. So this return to normalcy has been dishing out huge losses to investors who’d bought long-term bond funds or long-term bonds in the era of QE. Investors that own these way-under-water 30-year bonds outright can choose to hold the bonds to maturity at around 2050, when they will get face value back, and collect 1.5% or 1.8% coupon interest along the way.

Future bond buyers are looking at these juicy yields, and they’re licking their chops, hoping that yields will rise further to hit some magic number, at which point they’ll jump in, forming part of the demand for those bonds. There will always be enough buyers if the yield is high enough. And current bond buyers find those yields juicy enough, and a lot of demand emerges at 5%.

But investors that bought during QE are in a world of hurt. The iShares 20+ Year Treasury Bond ETF [TLT], which focuses on Treasury bonds with a remaining maturity of 20 years or more, fell another 1.6% today at the moment and has plunged by 51% from the peak in August 2020, which had marked the peak of the 40-year bond bull market that had turned into the biggest bond bubble ever (data via YCharts).

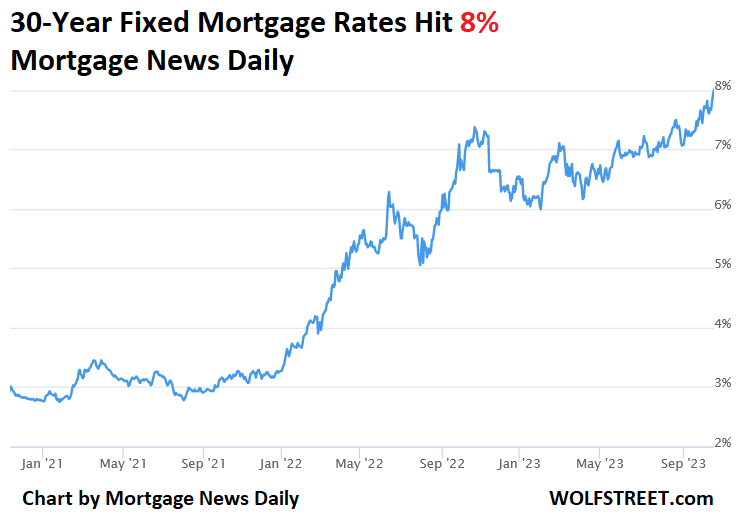

The 8% mortgage rates are here.

The average 30-year fixed mortgage rate kissed 8% today, according to the daily measure by Mortgage News Daily. If mortgage rates stay there to enter the weekly averages at that level, it would be the highest since 2000. Ah, the good old times are coming back?

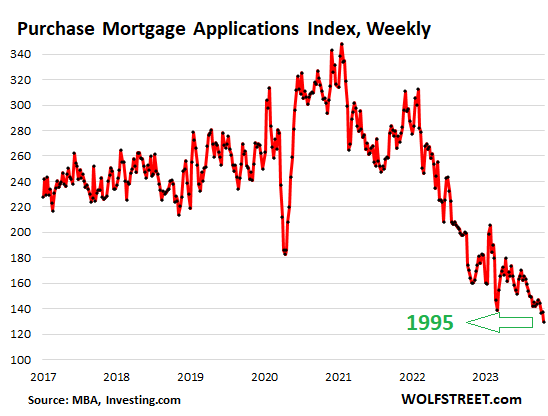

Housing market in deep freeze.

Mortgage applications to purchase a home have been on a steady collapse-track and in the last reporting week slid another 6% from the prior week to hit a new multi-decade low, and are 48% below the same week in 2019, according to data from the Mortgage Bankers Association today.

Mortgage applications to purchase a home are an indication of where home sales volume will be over the next few weeks. And home sales volume has already collapsed, and mortgage applications indicate that it will continue on this trend.

These 8% mortgage rates worked just fine back when prices were a lot lower. But prices have spiked in recent years, as the Fed repressed mortgage rates with QE and 0% short-term rates. And the resulting sky-high prices are impossible to make work with these mortgage rates.

In other words, the Fed-repressed mortgage rates have triggered a huge bout of home price inflation, and the surge in mortgage rates has now started to unwind it.

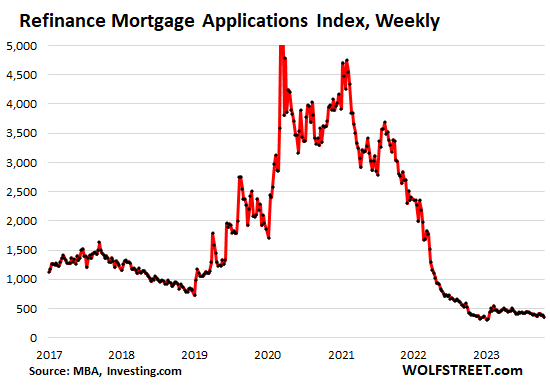

Mortgage applications to refinance a home plunged 10% for the week and were down by 87% from the same week in 2019, according to the MBA.

Most of the refis are cash-out refis, with non-cash-out refis having essentially vanished – they’re down about 97% from the same week in 2019, according to AEI Housing Center.

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter October 18th, 2023

Posted In: Wolf Street