ALWAYS CONSULT YOUR INVESTMENT PROFESSIONAL BEFORE MAKING ANY INVESTMENT DECISION

June 14, 2023 | Powell on the New Hawkishness in the Dot Plot and on Inflation: “We See that it Tells Us that We Need to Do More”

Wolf Richter

Renewed hawkish sentiments are building up at the Fed for the second half this year. That’s what we saw today. While the Fed kept rates steady today “to assess additional information and its implications for monetary policy,” the median projection in the FOMC’s infamous “dot plot” today calls for two more rate hikes this year, bringing the top of the range to 5.75%.

Of the 18 members, only two projected keeping rates the same, and 16 projected one or more rate hikes, going up all the way to one member projecting 1 full percentage point in hikes, according to the dot plot (my detailed discussion here).

Powell pointed at it right up front at the press conference in the prepared remarks: “Nearly all committee participants expect that it will be appropriate to raise interest rates somewhat further by the end of the year,” he said.

“Perhaps more restraint will be necessary than we had thought at the last meeting,” he said, pointing at the dot plot’s projections for core PCE inflation that moved up, for GDP growth that moved up, and for unemployment that moved down.

Forget rate cuts this year. Powell emphasized at the press conference that no committee member projected a rate cut on the dot plot: “I think as anyone can see, not a single person on the committee wrote down a rate cut this year, nor do I think it is at all likely to be appropriate if you think about it.” So he brushed that off the table entirely.

July would be a “live meeting,” Powell said twice at the post-meeting press conference, to make sure everyone got it, meaning the first of those rate hikes could happen at the next FOMC meeting in July.

In terms of pausing and then un-pausing, the Fed isn’t blazing any trails here. The Bank of Canada hiked last week after its pause since March, on resurging inflation fears; and the Reserve Bank of Australia, hiked for the second time since its pause, on inflation fears and surging labor costs without productivity gains. So maybe that’s the new pattern.

Powell said all kinds of worrisome stuff about inflation.

Core inflation “has not really moved down. It has not reacted much to our existing rate hikes. We’re going to have to keep at it,” he said.

“If you look at core PCE inflation over the last six months, you’re not seeing a lot of progress. It’s running at a level over 4.5%, far above our target and not really moving down. We want to see it moving down decisively, that’s all.”

“We don’t think we’re there with inflation yet… If you look at the full range of inflation data, particularly the core data, you just aren’t seeing a lot of progress over the last year,” he said.

“Headline inflation has come down materially, but we look at core as a better indicator of where inflation overall is going.”

“What we’d like to see is credible evidence that inflation is topping out and then getting it to come down.”

“We’re two-and-a-quarter years into this, and forecasters, including Fed forecasters, have consistently thought inflation was about to turn down and typically forecasted that it would, and been wrong.”

“Of course we are going to get inflation down to 2% over time. We want to do that with the minimum damage we can to the economy, of course. But we have to get inflation down to 2% and we will. And we just don’t see that yet.”

“Look at core inflation over the past six months, a year. You’re not seeing the kind of progress we want to see.”

“I still think, and my colleagues agree, that the risks to inflation are to the up side still.”

“Every year for the past three years, it [the median core PCE projection] has gone up over the course of the year. And it’s doing that again. We see that, and we see that inflation forecasts are coming in low again. And we see that it tells us that we need to do more.”

“We’re committed to getting inflation down. And that’s the number one thing. So that’s how I think about it.”

Why slow the pace of rate hikes on the way to the “destination?”

“It seems to us to make obvious sense to moderate our rate hikes as we got closer to our destination. The decision to consider not hiking at every meeting and to hold rates steady at this meeting is a continuation of that process.”

“The main issue that we’re focused on now is determining the extent of additional policy-firming that may be appropriate to return inflation to 2% over time.”

“So the pace of the increases and the ultimate level of increases are separate variables, given how far we have come.”

“It may make sense for rates to move higher, but at a more moderate pace.”

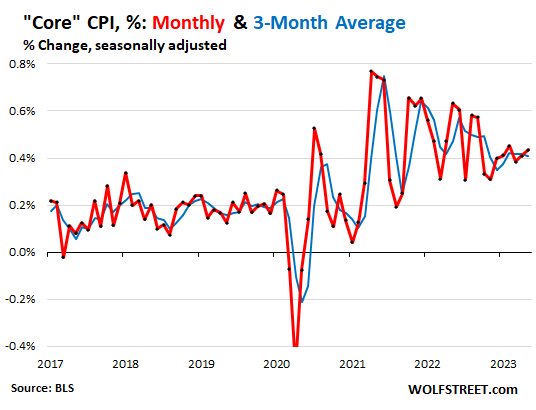

Here is what Powell was talking about in terms of core inflation not having moved down.

What Powell means: core inflation “has not really moved down.”

On a month-to-month basis, core CPI ticked up in April and May. The three-month average hasn’t moved down at all in seven months, running at an annualized rate of over 5%. Month-to-month, three-month-average, and six-month average measures are what Powell is referring to, not the year-over-year rates, which are skewed by the base effect.

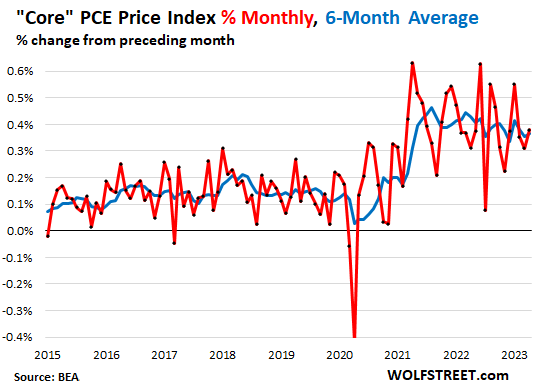

The month-to-month core PCE price index, and its six-month average, which Powell specifically referred to, also ticked up in April and is running at an annualized rate of 4.7%, roughly the same since July 2022:

STAY INFORMED! Receive our Weekly Recap of thought provoking articles, podcasts, and radio delivered to your inbox for FREE! Sign up here for the HoweStreet.com Weekly Recap.

Wolf Richter June 14th, 2023

Posted In: Wolf Street