The segment below offers a good big-picture overview of the interplay between incomes, consumer spending, economic growth and home prices. Canadian data looks worse than the US, but, so far, Canadian banks have allowed negative amortization to compound principal higher where payments are insufficient to cover principal and interest payments. Many variable-rate borrowers have had their amortization period extended well beyond 30 years in the process. Extend and pretend cannot continue indefinitely; a pick up in forced sales looks inevitable as unemployment ticks higher.

Bank of America just reported a big slowdown in consumer spending in America. Which is a major 2023 recession warning. And suggests that we could see job losses spike in future months with home prices and stock prices declining. Consumer spending on Bank of America credit/debit cards declined most in Furniture, Home Improvement, and Luxury Goods. While spending still rose for restaurants. Overall, spending was down -1.2% YoY from last April. Declining consumer spending is a big problem for the US Economy because 70% of GDP comes from spending. So it means our economy is decline. And likely that businesses will continue to lay off workers in 2023.

Another company that had a concerning report was Airbnb. Their stock price is down by 15% in the last week because they had a “muted” outlook for travel demand in the rest of 2023. A slowdown in Airbnb bookings would mean that certain housing markets might have issues. The ones with the biggest drops in occupancy include Miami, Philadelphia, Fort Lauderdale, Austin, San Antonio, and Cape Coral. Here is a direct video link.

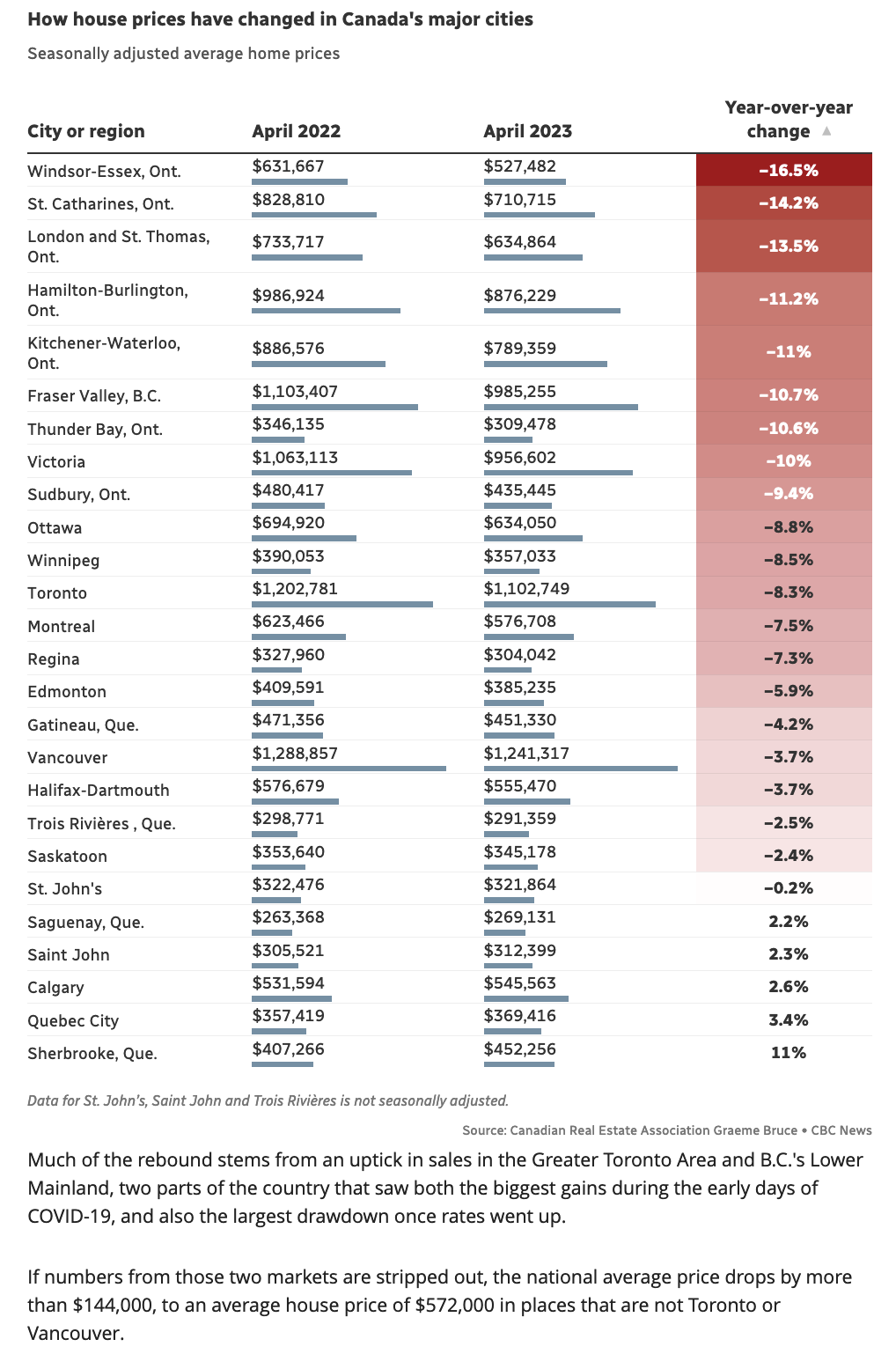

For repricing progress to date in major Canadian cities, see more here: Average Canadian home price $716,000 in April.